How to Exploit the

‘Great Gold Lag’

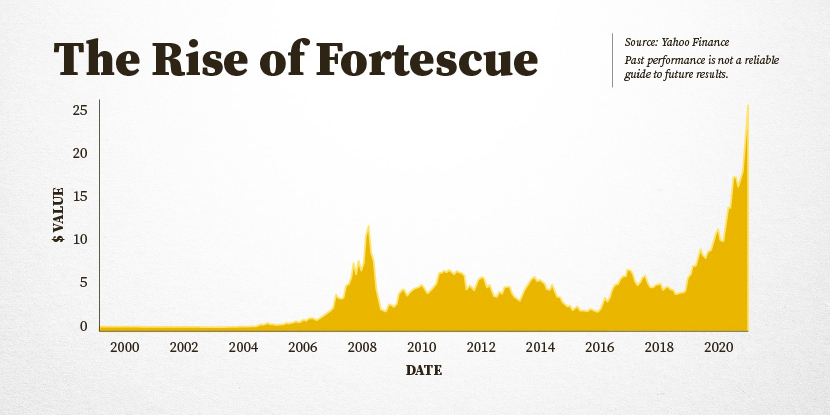

The 2003–2011 boom turned four mid-sized miners into global

powerhouses. Bringing early share investors along for the ride.

Who might be next? See below…

Welcome to

The Gold Digger Summit

This event will go live at 12:00pm (AEDT) sharp.

Days

Hours

Minutes

Seconds

$99 is all you need to pay upfront to get immediate access Diggers and Drillers…and to download James Cooper’s NEW Big 4 report immediately.

$99 is all you need to pay upfront to get immediate access Diggers and Drillers…and to download James Cooper’s NEW Big 4 report immediately.

So why not have a look at it?

So why not have a look at it?